US Stocks Rally Despite Weak Data

Further US Data Weakness

US equities are continuing to push higher on Friday as the US Dollar drifts further lower following lacklustre data yesterday. Headline US retail sales were seen printing just 0.1%, down from 1.7% prior, with core retail sales also seen at 01%, down from 0.8% prior. Alongside these readings, headline PPI was seen falling 0.5% last month, down from 0% the month before and below the 0.2% reading the market was looking for. Core PPI was also down on the month at -0.4% from 0.4% prior, below the 0.3% the market was looking for.

Fed Easing Expectations

Coming on the back of the weaker US inflation data we saw earlier in the week, the data adds to a sense of softening US economic activity, putting focus back on Fed easing expectations. Indeed, pricing for a cut as early as July has started to move higher again following the data, now sitting around 35%. Speaking at the start of a two-day conference yesterday, Fed chair Powell warned "We may be entering a period of more frequent, and potentially more persistent, supply shocks—a difficult challenge for the economy and for central banks."

Near-Term View

Looking ahead, equities look likely to remain supported while USD continues to drift lower. Residual optimism around a potential US/China trade deal and growing Fed rate-cut expectations should continue to support stocks though any sign of a breakdown in US/China trade relations could see sentiment deteriorate quickly.

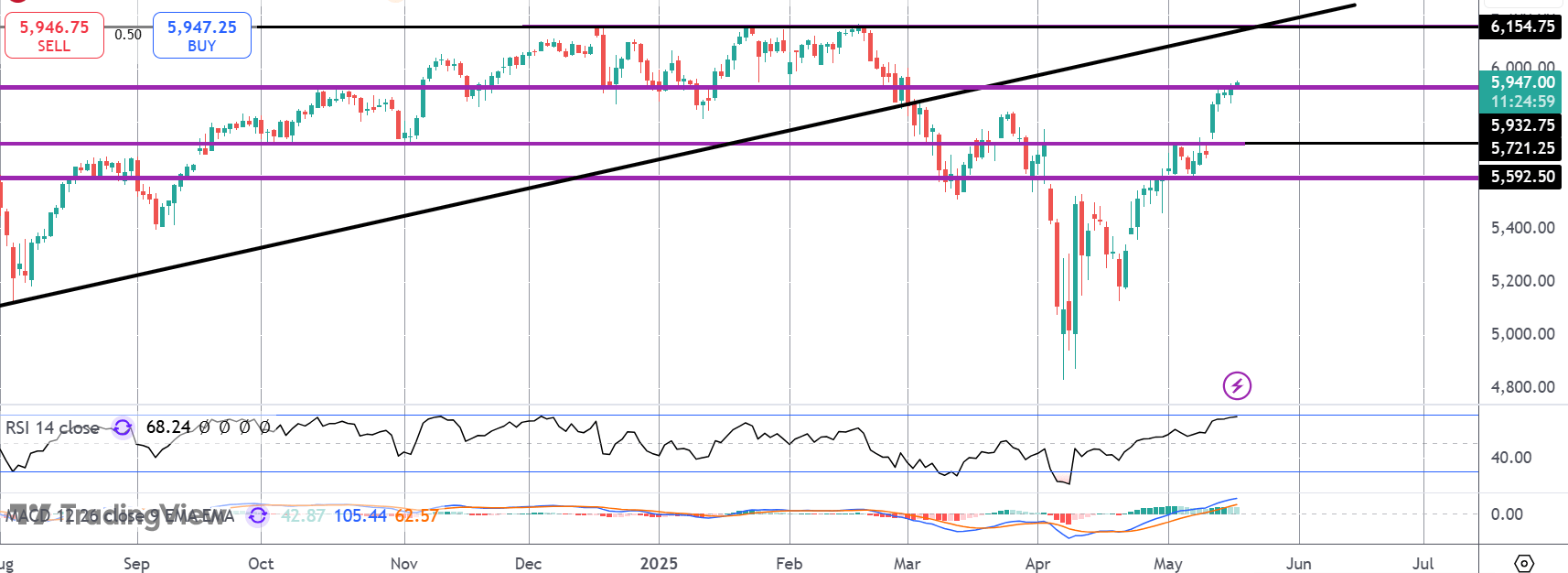

Technical Views

S&P 500

The rally in the S&P has seen the market breaking out above the 5,721.25-level with price now testing above the 5,832.75-level today. With momentum studies bullish, focus is on a continued push higher towards the 6,154.75-level next and a retest of the underside of the broken bull trend line.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

With 10 years of experience as a private trader and professional market analyst under his belt, James has carved out an impressive industry reputation. Able to both dissect and explain the key fundamental developments in the market, he communicates their importance and relevance in a succinct and straight forward manner.