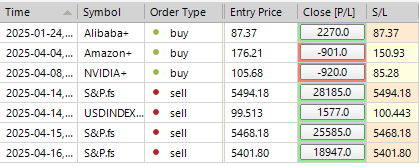

SP500 LDN TRADING UPDATE 22/04/25

SP500 LDN TRADING UPDATE 22/04/25

WEEKLY BULL BEAR ZONE 5250/60

WEEKLY RANGE RES 5349 SUP 5019

DAILY ONE TF DOWN 5262

WEEKLY ONE TF DOWN 5496

MONTHLY ONE TF DOWN 5997

WEEKLY ACTION AREA VIDEO TO FOLLOW AHEAD OF NY OPEN

GOLDMAN SACHS TRADING DESK VIEWS

U.S. EQUITIES UPDATE: SEA OF RED

Date: 21 April 2025

Key Indices Performance:

- S&P 500: Down 2.36%, closing at 5,158.

- Nasdaq 100 (NDX): Down 2.46%, closing at 17,808.

- Russell 2000 (R2K): Down 2.22%, closing at 1,839.

- Dow Jones Industrial Average: Down 2.48%, closing at 38,170.

Trading Volume:

- Total shares traded: 13.8 billion, below the year-to-date daily average of 16.3 billion.

Market Volatility:

- VIX increased by 13.93% to 33.78.

- Crude oil fell by 1.92% to $63.44.

- U.S. 10-Year Treasury yield rose by 0.08% to 4.40%.

- Gold surged by 2.82% to $3,420, marking a new all-time high.

- Dollar Index (DXY) decreased by 0.80% to 98.35.

- Bitcoin rose by 2.50% to $87,240.

Market Overview:

- Markets opened the week with significant declines; the S&P 500 recorded its third drop in four sessions, while the Nasdaq is down four consecutive sessions.

- Trading activity was subdued due to several international market closures.

- The S&P's top-of-book liquidity remains weak, with E-mini futures depth around $3 million, while ETF trading volume is stabilizing at approximately 31%.

- Broad market weakness was observed with 463 S&P companies closing lower, notably large-cap tech stocks like NVIDIA and Tesla, both down 4-5%.

Currency and Commodities:

- The U.S. Dollar and Gold continue to attract attention; the Dollar Index is at its lowest since April 2022, while Gold exceeds $3,400 per ounce.

Political and Economic Context:

- Tensions persist between President Trump and Federal Reserve Chair Powell, with Trump advocating for preemptive rate cuts to prevent an economic slowdown.

- Buyback blackout period ends this Friday, with expectations for CTA buying across the board.

Key Levels and Events:

- S&P 500 pivot levels: Short-term at 5,595, Medium-term at 5,775, Long-term at 5,479.

- Upcoming releases include flash PMIs on Wednesday and the final University of Michigan consumer sentiment report on Friday, along with several Federal Reserve speakers.

Market Flows:

- Overall activity was moderate, rated 4 out of 10. The market showed a -1.83% sell skew, driven mainly by long-only investors selling tech, macro products, healthcare, and discretionary sectors, while buying financials and energy.

- Hedge fund flows were balanced, with a notable decrease in short covering since July 2024.

Derivatives Market:

- Options activity was limited as markets declined. Volatility was bought on the drop, and skew was significantly impacted.

- Downside volatility underperformed, indicating limited panic despite aggressive selloffs.

- Some short-dated downside buying occurred in the morning, with September upside purchases towards the day's end as markets rebounded.

Upcoming Events:

- Approximately 23% of S&P 500 market recap reports are due this week.

- The IMF and World Bank Spring meetings are happening, with numerous international officials in Washington, leading to potential headlines on trade and tariff negotiations.

Market Outlook:

- The options straddle for the remainder of the week is approximately 3%.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!