Institutional Insights: Credit Agricole FX Weekly 18/7/25

Calling the ECB’s global EUR bluff?

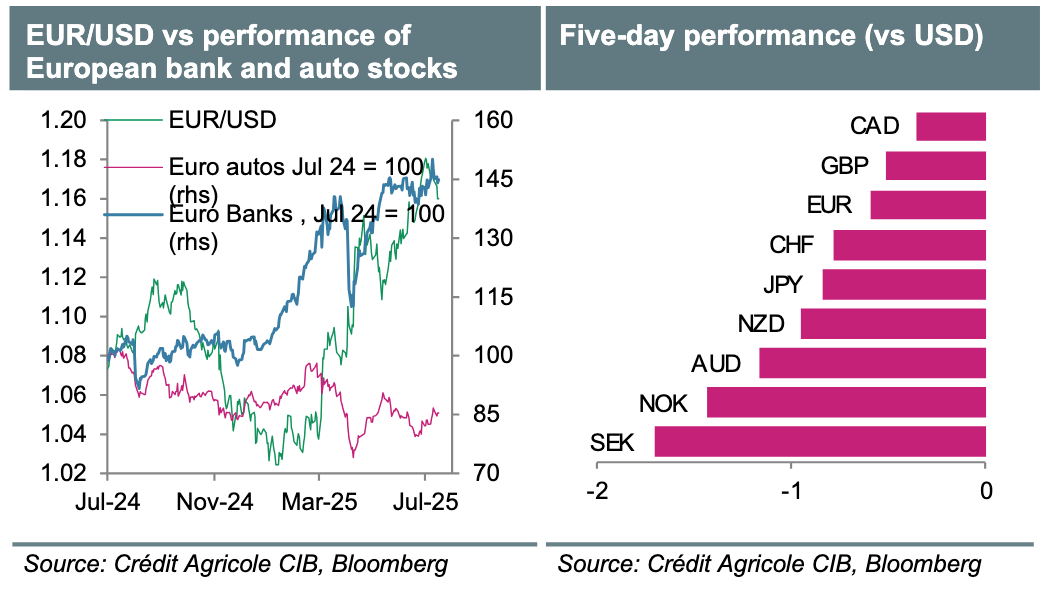

Recent feedback from European clients underscores growing concerns among investors and corporates about the impact of the EUR’s recent strength on the Eurozone’s economic outlook. Specifically, clients fear that aggressive currency appreciation could undermine the region’s international competitiveness, exacerbating the negative effects of U.S. trade tariffs and intensifying competition from manufacturing exporters such as China.

Interestingly, these client perspectives appear to contrast with the European Central Bank’s (ECB) recent efforts to bolster the global profile of the EUR, which indirectly supports currency appreciation. This divergence is further reflected in market dynamics: the EUR’s rapid appreciation aligns with strong performance in Eurozone bank stocks, traditionally seen as indicators of domestic economic health. Conversely, the EUR has largely decoupled from underperforming car manufacturer stocks, which are proxies for the health of Eurozone exporters.

Looking ahead to next week, we anticipate the ECB will maintain its current interest rates while adopting a cautiously optimistic tone regarding the Eurozone’s domestic economy. However, the ECB is likely to acknowledge ongoing downside risks stemming from global trade uncertainties and geopolitical tensions. President Christine Lagarde may continue advocating for the EUR’s global role but could also recognize the potential risks posed by its strength.

FX investors will be closely monitoring Eurozone manufacturing PMIs for July, which serve as indicators of export sector health, alongside services PMIs and Germany’s ifo business climate index, both of which reflect domestic economic conditions. Any disappointing data could underscore the self-defeating nature of further EUR gains and prompt investors to question the ECB’s stance on promoting the global EUR.

In Japan, attention is shifting to the 20 July Upper House election, where economists estimate that the LDP-Komeito coalition may secure only 46 seats, potentially losing its majority. Such an outcome could heighten political uncertainty and accelerate a shift away from fiscal austerity, raising sovereign credit concerns and weighing on the JPY. Additionally, next week’s Tokyo CPI data for July will be closely watched for further economic insights.

FX Outlook

EUR/USD Outlook

While we have recently adopted a more constructive stance on EUR/USD in the near term, we remain skeptical that the euro has significant room for further gains from current levels in 2025. We anticipate renewed EUR/USD weakness in 2026. Recent support for the euro has largely stemmed from market expectations that it could benefit from diversification away from the USD. Additionally, optimism surrounding aggressive fiscal stimulus in the Eurozone boosting economic prospects and attracting capital inflows has supported the EUR. These factors may sustain EUR/USD for the remainder of the year. However, many positives appear priced into the EUR, as indicated by short- and long-term fair value models, which could limit future gains and amplify downside risks within the next 6 to 12 months.

USD Outlook

The USD outlook for 2025 may remain subdued due to concerns over the impact of the Trump administration’s policies on the US economy and USD assets. This could lead to portfolio rebalancing away from the US and an increase in short-USD hedges. Additionally, the fiscal stimulus package and the need to raise the debt ceiling may negatively affect long-term US public finances. However, we do not foresee a USD collapse, as the economic impact of Trump’s policies is expected to be significant but transitory. The US economy could begin recovering in H225 and rebound in 2026, with a shift in focus from trade to fiscal stimulus policies. This recovery could allow the Fed to avoid aggressive policy easing, especially if inflation remains persistent. We also doubt the USD will lose its reserve currency status, and we expect a gradual recovery in the next 6 to 12 months.

EUR/CHF and CHF Outlook

Tariff uncertainties have fueled demand for safe havens like the CHF, strengthening it even against the resurgent EUR. While EUR/CHF may edge higher throughout the year with the return of ZIRP in Switzerland making CHF an attractive funding currency, lower inflation differentials could temper CHF real valuations. Additionally, balanced growth prospects should help avoid large nominal losses.

JPY Outlook

We remain skeptical about major trade deals being signed between the US and its trading partners, making the JPY a valuable hedge against potential stagflation in the US. Asset managers continuing to diversify away from US and Japanese assets could benefit the JPY. The exchange rate may face downward pressure from the Fed cutting rates and the BoJ hiking rates, though the latter is unlikely until 2026.

GBP Outlook

Recent developments have increased downside risks to the UK economic outlook, prompting a more dovish BoE stance. Key factors include the failure of welfare reform under Keir Starmer’s government, disappointing UK economic data, and the BoE’s acknowledgment of a growing negative output gap. Despite these challenges, several negatives are already priced into GBP: (1) we expect the bank rate to reach 3.5% in 2026, slightly above current market expectations; (2) concerns about UK fiscal outlook are unlikely to escalate into fears of creditworthiness; and (3) GBP appears undervalued against the EUR and fairly valued against the USD. We maintain that GBP should recover some ground against EUR and USD in H225 and outperform EUR in 2026.

USD/CAD Outlook

USD/CAD has returned to levels near 1.36 due to broad USD selling, surpassing what relative rates would suggest. Any potential trade agreement between the US and Canada could serve as a catalyst for a spot pullback. With investor concerns about US tariffs and global trade wars likely peaking, the focus may narrow to US-China trade tensions, which would have less impact on the AUD compared to a broader trade war.

AUD and NZD Outlook

China’s government is expected to continue stimulating its economy to counter the growth drag from US tariffs, benefiting the AUD due to its strong correlation with the CNY. Australia’s rate market appears overly aggressive in pricing rate cuts, as the tight labor market and higher government spending post-election are likely to support inflation. Meanwhile, New Zealand’s economy is recovering from a deep recession, aided by strong agricultural export prices and production. While US failure to sign major trade deals could negatively impact the NZD, diversification away from US assets will likely support NZD/USD, which remains positively correlated with Asia-US equity market performance.

NOK and SEK Outlook

The NOK faces challenges on its recovery path, as evidenced by April’s correction. However, Norway’s robust fundamentals and the currency’s rate appeal, despite Norges Bank’s frontloaded easing, suggest further long-term appreciation—assuming no major global disruptions. The SEK has emerged as the surprising YTD outperformer among G10 FX, leveraging its high-beta EUR proxy status. However, a softer economic patch and potential easing may hinder gains unless Sweden’s macroeconomic performance convincingly outpaces the Eurozone.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!