Daily Market Outlook, October 31, 2023

Daily Market Outlook, October 31, 2023

Munnelly’s Market Commentary…

Asia - stock markets experienced mixed trading as the month came to a close. This period was marked by a significant influx of data releases, including discouraging official Chinese PMIs, and investors also had to digest a multitude of earnings reports, along with the conclusion of the Bank of Japan's live meeting. The Nikkei 225 initially had a volatile session, with Industrial Production and Retail Sales missing expectations. However, it later found support following the Bank of Japan's policy announcement, which turned out to be less aggressive than initially anticipated. On the other hand, the Hang Seng index dropped significantly by 2.0%, while the Shanghai Composite was down by 0.3%. This decline came as a response to disappointing PMI data that indicated China's factory activity had slipped into contractionary territory for October. Additionally, the market was influenced by a slew of earnings releases from major corporations such as Bank of China, BYD, and PetroChina. Overall, the region's markets faced a complex mix of factors, including economic data, corporate earnings reports, and the outcome of central bank policy decisions.

Europe - In the UK, the British Retail Consortium's (BRC) shop price index for October fell to 5.2%, down from 6.2% in September. This decrease marked the lowest level in over a year.

The October Lloyds Business Barometer, released earlier today, showed a rebound in overall business confidence to its second-highest level for the year. This rise effectively offset more than half of the slide observed in September. Notably, business confidence remains significantly above its long-term average. The improvement in sentiment extended to both the general economy and businesses' own prospects. The retail and services sectors played a pivotal role in driving this rebound, and eight of the twelve UK regions or nations reported increased business confidence. Furthermore, firms expressed greater positivity about hiring prospects for the year ahead, wage expectations remained elevated, and a rising number of businesses expected to increase prices.

In the Eurozone, GDP data for Q3 is expected to indicate no change in economic activity. Earlier releases for Spain and Germany were slightly better than anticipated, with Spain showing a 0.3% quarterly increase and Germany recording a -0.1% change. This has reduced the risk of a Eurozone output decline. Annual headline Consumer Price Index (CPI) inflation in the Eurozone is anticipated to have significantly eased in October. The forecast indicates a decline in the annual rate to 3.1% from the 4.3% reported in September, primarily driven by the base effects from last year's surge in energy prices. Core inflation is also expected to decrease, albeit more modestly, with a drop to 4.3% from 4.5%. Lower-than-expected figures from Germany and Spain introduce some downside risks to these forecasts.

US - Stateside, The quarterly US Employment Cost Index (ECI) will provide insight into wage growth in advance of Wednesday's US monetary policy update. The ECI is a more comprehensive but less timely indicator than the monthly labour market report. The forecast suggests a 1.1% increase in Q3, up from 1.0% in Q2, though lower than the figures seen in Q1 and the average for the previous year. This data supports the notion that US wage growth has slowed, even in a tight labour market.

FX Positioning & Sentiment

On Tuesday, the JPY weakened and hovered near a one-year low against the US dollar. This followed the Bank of Japan's (BOJ) decision, which was viewed as a small step toward ending years of massive monetary stimulus, but it disappointed some investors who had expected a more significant move. At the conclusion of its two-day policy meeting, the BOJ announced that it would maintain the 10-year government bond yield around 0% as part of its yield curve control (YCC) framework. However, it redefined 1.0% as a flexible "upper bound" rather than a rigid cap. Additionally, the BOJ removed its commitment to defend the yield level with offers to buy an unlimited amount of bonds. While some analysts interpreted this as a de facto dismantling of the BOJ's YCC regime, the yen still depreciated by approximately 0.8%, breaching the 150 yen per dollar threshold and reaching an intraday low of 150.26.

CFTC Data As Of 27-10-23

USD net spec long up a touch in Oct 18-24 period; $IDX rose 0.03% in period

Since period closed ECB dovish hold & Japan CPI may moot period adjustments

EUR$ +0.12% in period, specs -2,843 contracts; weak growth trump inflation

$JPY +0.05%, specs +3,029 contracts now -99,629; pair hovers near 150

GBP$ -0.16% in period specs -18,636 contracts; dovish BoE rate view weighs

AUD, NZD net spec short grew amid low rates, growth view; weak China growth

$CAD +0.67% in period, weak glbl growth and stagnant BoC rates weigh

BTC +18.2% period, specs sell 781 contracts flip to short, BTC steady since

End of developed mkt hikes and global growth remain key determinants ( Source Reuters)

FX Options Expiries For 10am New York Cut

(1BLN+ represent larger expiries, more magnetic when trading within daily ATR)

EUR/USD: 1.0400 (746M), 1.0410-20 (578M), 1.0450 (1.8BLN)

1.0485-90 (467M), 1.0500 (1.6BLN), 1.0525-35 (1.7BLN)

1.0540-50 (1.3BLN), 1.0560 (250M), 1.0575-80 (748M)

1.0590-00 (1.51BLN), 1.0610-25 (943M), 1.0640-50 (1.29BLN)

1.0700-10 (923M)

USD/JPY: 148.60-70 (847M), 149.90-00 (1.43BLN), 150.15 (262M)

USD/CHF: 0.9200 (370M). EUR/CHF: 0.9170 (929M)

0.9370 (800M)

GBP/USD: 1.2150-60 (548M). NZD/USD: 0.5850 (741M)

AUD/USD: 0.6120 (533M), 0.6185 (200M), 0.6250 (250M)

0.6330 (566M), 0.6360 (245M), 0.6415 (231M)

USD/CAD: 1.3700 (242M), 1.3800 (224M), 1.3825 (615M)

1.3900 (359M). USD/ZAR: 18.50-56 (712M), 18.80 (209M)

Overnight Newswire Updates of Note

BoJ Makes 1.0% Its New 10-Year JGB Yield Reference Point

Yen Weakens Past 150 Against Dollar After BoJ Tweaks Policy

Japan September Jobless Rate Falls To 2.6%

Japan September Retail Sales Rise 5.8% Year-On-Year

Japan Industrial Production Growth Misses Consensus Ahead

China Factory Activity Logs Surprise Decline In October

US Tsy Cuts Quarterly Borrowing Estimate To $776 Bln

BoC Gov. Macklem: Economy Enters Weaker Phase

World Bank Warns Oil Price Could Soar To Record $150/Bbl

Samsung Electronics’ Third-Quarter Net Profit Beats Consensus

Tesla Closes Below $200, Hits 5-Month Low As A Tough October Rolls On

Apple Unveils New Laptops, iMac And Trio Of More Powerful Chips

Nvidia’s $5 Bln Of China Orders In Limbo After Latest US Curbs

(Sourced from Bloomberg, Reuters and other reliable financial news outlets)

Technical & Trade Views

SP500 Bias: Bullish Above Bearish Below 4100

Above 4160 opens 4200

Primary resistance is 4280

Primary objective is 4075

20 Day VWAP bearish, 5 Day VWAP bearish

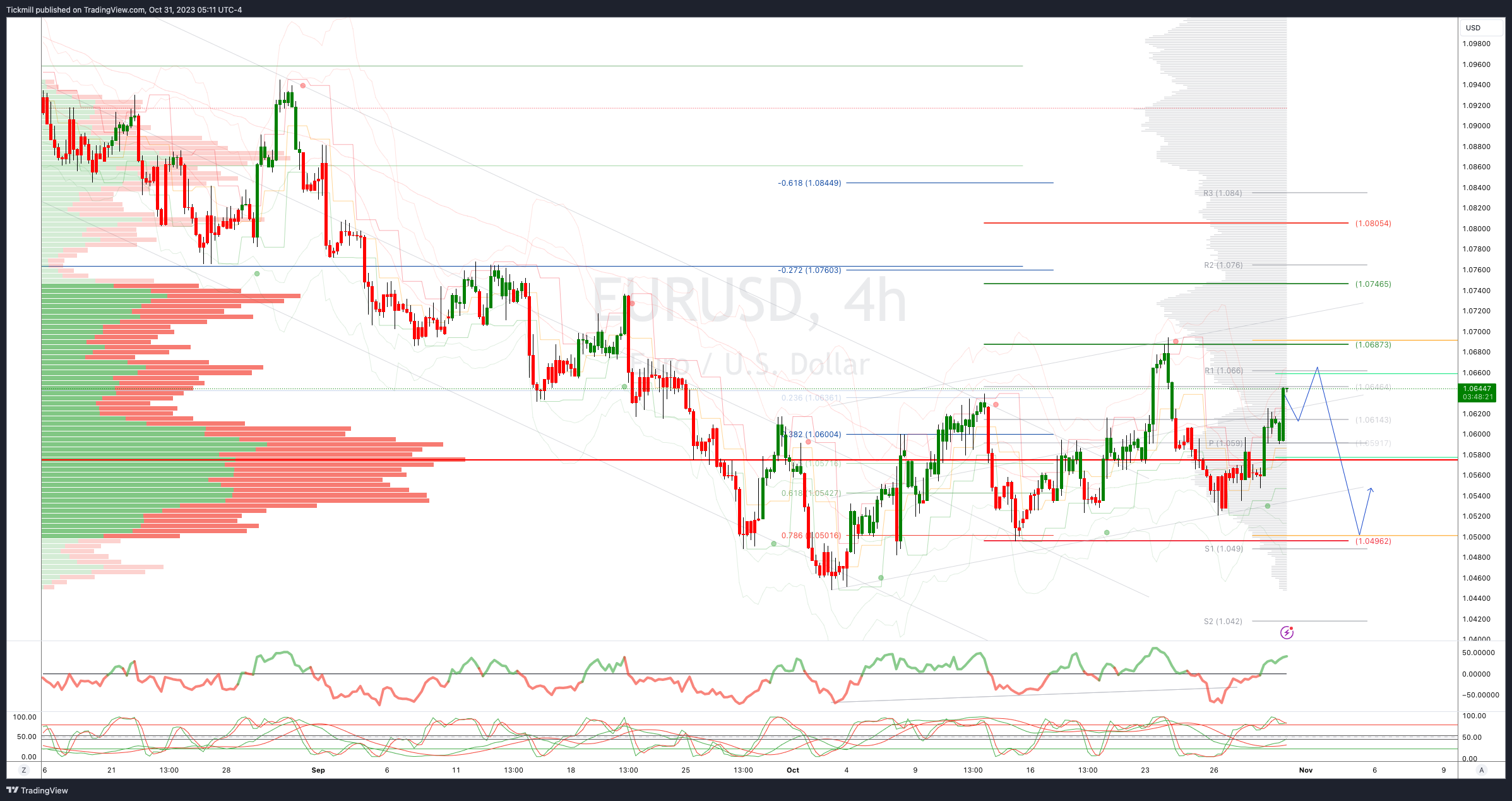

EURUSD Bias: Bullish Above Bearish Below 1.06

Below 1.0550 opens 1.0480

Primary support is 1.05

Primary objective is 1.04

20 Day VWAP bearish, 5 Day VWAP bearish

GBPUSD Bias: Bullish Above Bearish Below 1.22

Below 1.21 opens 1.1950

Primary support is 1.21

Primary objective 1.24

20 Day VWAP bearish, 5 Day VWAP bearish

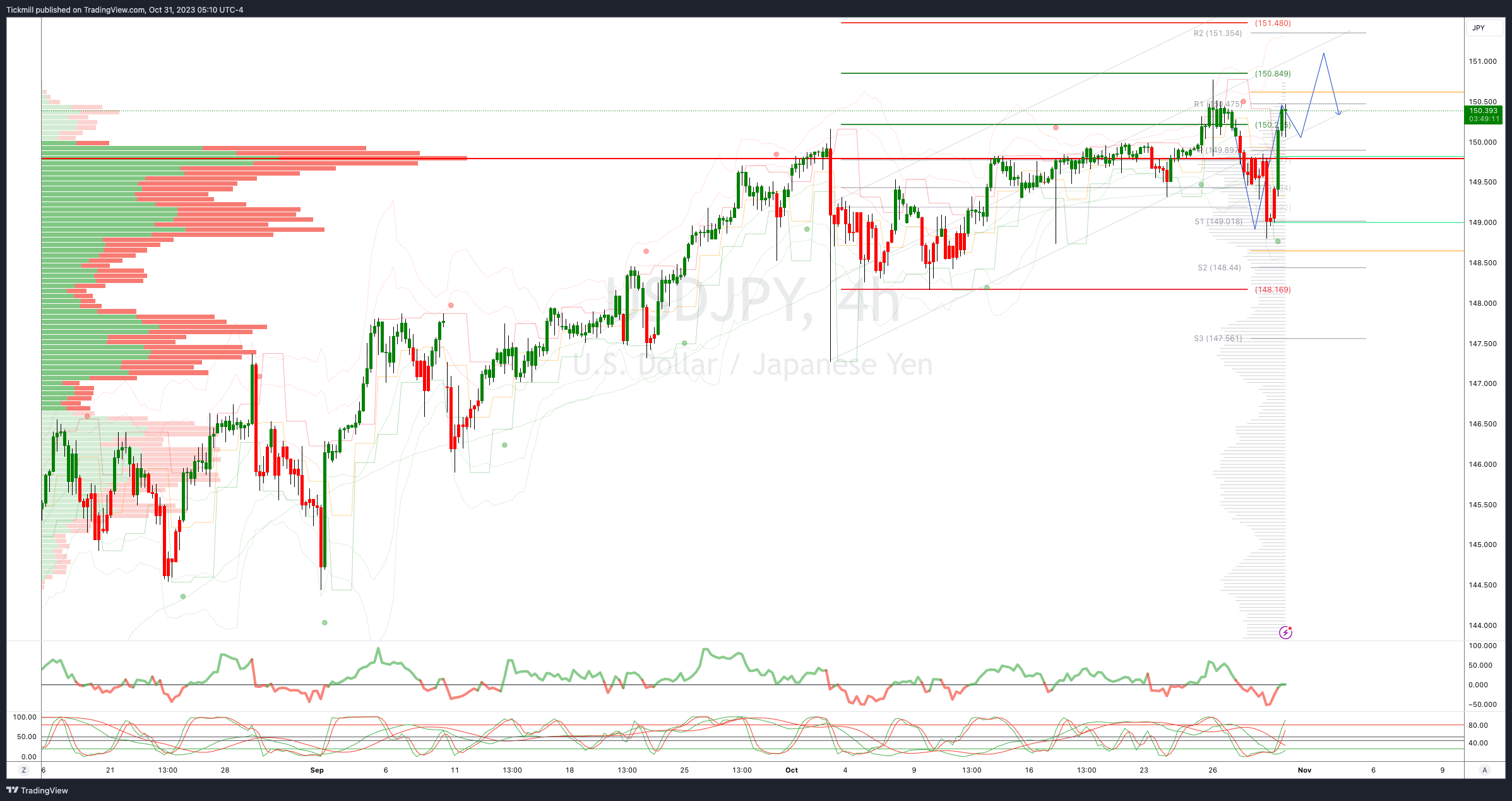

USDJPY Bias: Bullish Above Bearish Below 149.25

Below 149 opens 148.50

Primary support 144.50

Primary objective is 151

20 Day VWAP bullish, 5 Day VWAP bullish

AUDUSD Bias: Bullish Above Bearish Below .6400

Above .6475 opens .6525

Primary resistance is .6620

Primary objective is .6270

20 Day VWAP bearish, 5 Day VWAP bearish

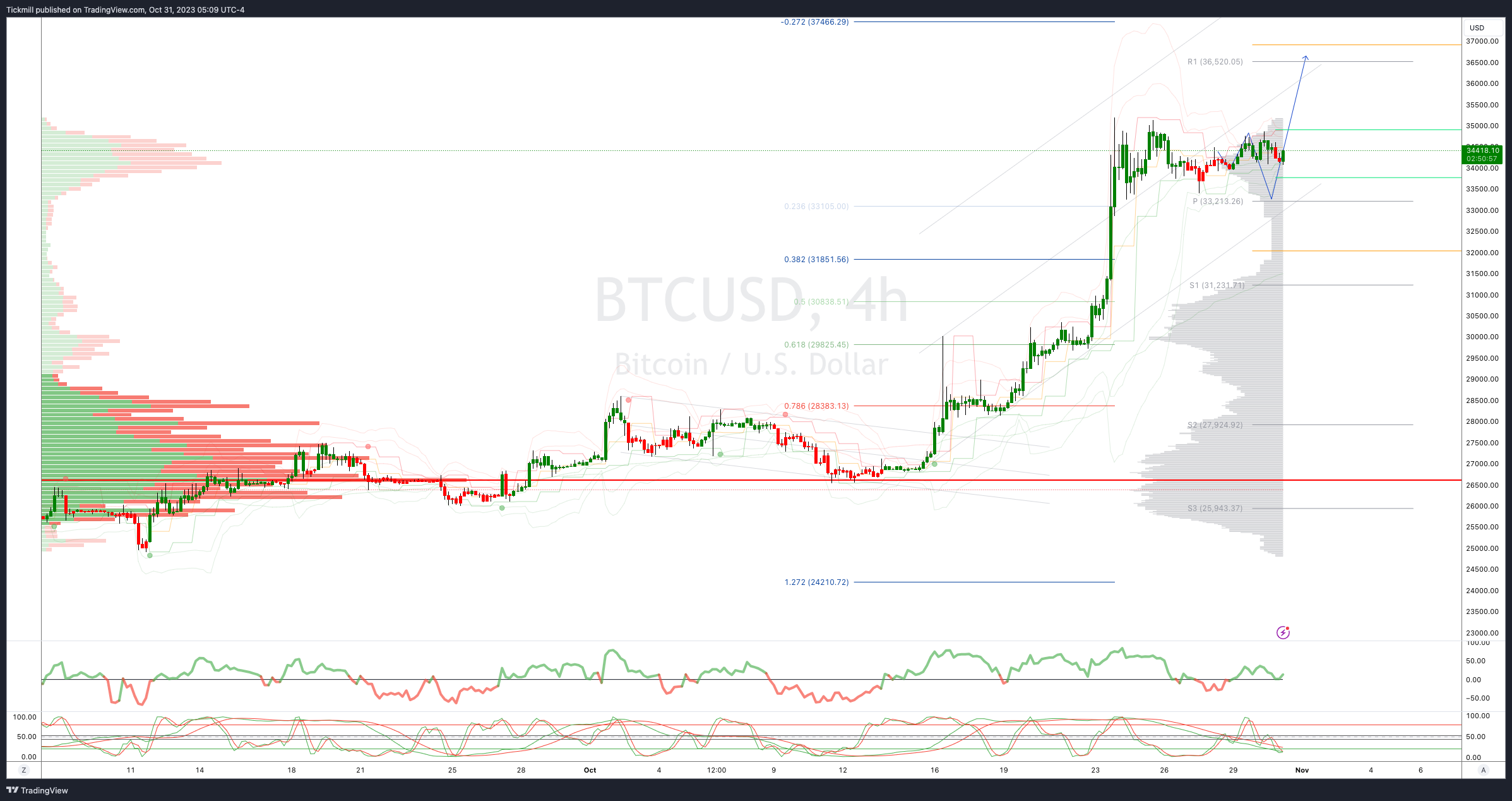

BTCUSD Bias: Bullish Above Bearish below 32000

Below 27100 opens 26500

Primary support is 30000

Primary objective is 37000

20 Day VWAP bullish, 5 Day VWAP bullish

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!